Bostoncoin update March-April 2023

Good news, everyone

BTC still holding strong: recent on-chain analysis indicates that 65% of BTC wallets have been holding their Bitcoin for over one year. Institutions and new buyers are going to have to bid the price very high to convince these long-term holders to sell.

Collapsed exchange FTX has allowed all investors in Japan to access their funds. Over $50 million has been paid to Japanese investors. We live in hope that other investors will get back some or all of the money that was locked up in 2022.

For those who are still keeping funds on an exchange: STOP IT!

(click this link for some comedy gold; click here to get a secure storage device)

We do not necessarily enjoy schadenfreude, the pleasure that comes from watching someone else come to harm; instead, we like to learn from the mistakes of others. It is certainly easier to learn from the mistakes of others, rather than going through the time to make the mistake yourself.

Many individual investors lost control of their coins when exchanges such as Celsius and FTX went down in 2022, but it was not just naïve individuals who lost their money. Several large crypto fund managers also lost big, with one fund manager recently admitting that they lost 91.4% in their main fund last year.

According to filings with the SEC, the MC fund was holding around US$9 billion in investor funds. Losing 91% of your assets would be bad for anyone; perhaps it is mildly reassuring to know that it also happens to billion-dollar hedge funds?

In past newsletters, we may have occasionally (harped on) mentioned the importance of Diversification. It seems that the failed crypto hedge fund (which we will not name) made a couple of mistakes:

1) diversification: they had too many of their assets stored on the FTX platform

2) diversification: they had too much invested in the FTT token (issued by FTX)

3) associated risk: they believed the lies of Sam Bankman-Fried (SBF of FTX)

The MC fund issued a letter to its investors, stating that they had learned their lessons and would do better in future. Among other improvements, the fund has decided to only retain funds on an exchange if they are to be sold within 48 hours; all tokens or coins intended to be held for the longer term will now be stored offline or with an independent custodian.

In related news, another crypto hedge fund that invested heavily with FTX, has lost “only” 51% of their investor funds, and has decided to close. The co-founder of Galois Capital issued a statement saying that it was no longer financially viable to run the fund, and has returned the remaining funds to investors.

We support the character of a fund manager who learns lessons and bows out gracefully. We will be watching the other (-91%) fund closely to see if they can bounce back. Godspeed to everyone who is acting with integrity in the space.

Comparing Hedge Funds

One of the largest hedge fund studies ever conducted has compared the experience of fund managers and the performance of cryptocurrency hedge funds to their traditional stock fund counterparts.

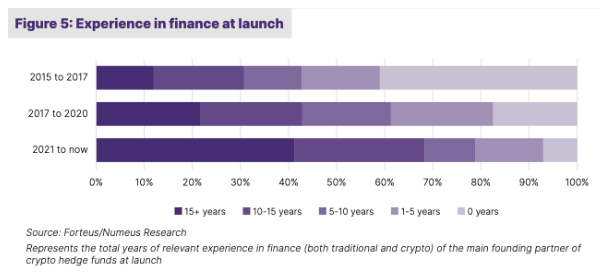

It seems that the crypto hedge fund industry has matured a lot in the last few years. Back in 2015-2017, over half the crypto fund managers had less than five years of experience in the markets (yes, Bostoncoin was around back then, with 20+ years of experience; we were in the less than 10% minority).

More recently, researchers note that over two-thirds of crypto fund managers now have 10-15+ years of experience, indicating that crypto hedge funds have been attracting talented people from traditional stock funds.

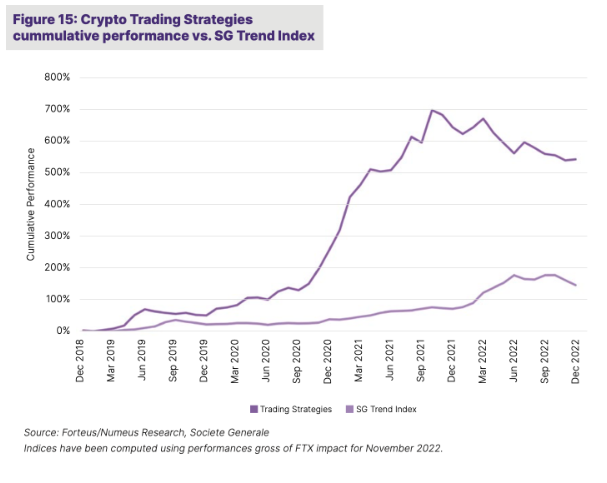

In performance studies, researchers at Numeus compare how traditional stock funds’ performance have fared versus crypto hedge funds over time. This is a great chart to show your friends Over a five-year timeframe, the average stock market hedge fund returned around 150%, whereas the average crypto hedge fund returned around 550%, almost four times better.

As crypto markets are yet unregulated and can be far more volatile than stocks, it would be unwise to unload all your stocks and put all of your funds into a crypto hedge fund. However, there is much to be said for the strategy of putting 5-10% of your entire portfolio into a good quality diversified crypto hedge fund to gain extra performance whilst limiting overall portfolio risk.

Bank collapses bad for cash, but good for crypto

Last month we witnessed the collapse of several US banks, including Silvergate, Signature and Silicon Valley Bank (SVB). Many people outside of the inner circles may not have heard of these three banks, but aside from lending to many Silicon Valley startup companies, SVB was also the sixteenth-largest bank in the USA.

As you will know, many banks lend to each other, so the collapse of a ‘top twenty’ bank may yet have ripple effects in the marketplace. A recent news report said that “up to 200” more banks may be affected*.

Although bank Federal Deposit Insurance (FDI) promises to cover deposits up to $250 000, this is a small figure when you consider that many large businesses held their operating capital and payroll inside SVB. Can you imagine having held millions or tens of millions in cash and the FDI says they will reimburse your business up to $250 000?

The obvious alternative for large businesses is to hold a maximum of $250 000 in many different bank accounts at different banks, but this can be an onerous task when you are trying to run a large organisation. Banks may be regulated, but as we have just seen, they are far from safe.

Some cynical no-coiners have pointed at the above three banks and suggested that they were at higher risk because they were involved with crypto companies, and so it is “crypto’s fault” for the bank collapses.

Reality may be harder to swallow, as it indicates that almost no bank is safe. Many banks take deposits in cash, hold a little for liquidity and invest the balance into (allegedly) “safe” assets such as government bonds. A couple of years ago, when prevailing pandemic interest rates were close to zero, the government bonds may have been guaranteed to pay 1-2% interest. Since interest rates have been rising the last few months, and you can get 3-4% anywhere, nobody wants to pay full price for a fixed-rate 2% government bond.

TLDR: when interest rates go up, the price of government bonds goes down. So, the local bank collapses can be seen as the fault of the Fed and Reserve Banks.

*UPDATE: First Republic Bank and Credit Suisse have just been bailed out, and more banks may yet be affected. Credit Suisse was bought by UBS for $3.25 billion; amazingly, Credit Suisse in 2006 was worth over $140 billion. How the mighty have fallen.

To help mitigate possible “bank runs” or further bank collapses, the Central Banks may have to inject further cash into the system (‘Quantitative Easing’ or QE). As we found from the 2008 Global Financial Crisis and the 2020 pandemic, turning on the cash printers can lead to hyperinflation, which the Fed and Central Banks can counter by raising interest rates. Raising rates can lead to bond losses, bank collapses, cash printing, hyperinflation and higher interest rates, which can lead to bond losses, bank collapses, cash printing, hyperinflation and so we go around again…

Remember that cryptocurrency was created by Satoshi Nakamoto in 2009 when the western banks were being bailed out for the second time. Satoshi had a vision of a currency that could not be inflated, minted, printed or manipulated by governments or anyone else. If anyone tells you that more bank collapses are imminent, or hyperinflation is the fifth horseman of the Apocalypse, just smile, say, “Bitcoin fixes this” and walk away.

What about government-issued digital currency?

As reported last month, many governments and nations around the world have either issued a centralised bank digital currency (CBDC) or are planning to do so. Thus far, twelve countries have an operational CBDC and fifty more nations have a CBDC in the pipeline. Note that due to their centralised nature and being under government control, these are not “crypto”-currencies, but “digital” currencies.

Although cryptocurrencies are tracked on a massive ledger system (the worldwide blockchain), crypto provides pseudo-anonymity: anyone can see where the coin came from or went, but they do not necessarily know the identity of the person sending or receiving it.

In contrast, a central bank digital currency can be tracked by the government, and even manipulated or confiscated by the issuer. As some have discovered with the Chinese CBDC, if you drop litter, the government can take funds from your digital wallet. There are rumours that a government currency could be manipulated “for your own good”, because someone with diabetes or obesity would not be able to buy junk food, or the government could restrict how much you spend on alcohol, cigarettes or other items.

“OK, but China is a Communist-quasi-Capitalist country run by a dictatorship,” we hear you say. “That type of financial control would not work anywhere else.”

Let’s have a look at what has happened in Nigeria. Nigeria is a democratic republic, the same non-dictatorial system of government as in the USA. Just like the USA, the Nigerian people are free to vote for their leaders. Aside from being a relatively poorer nation, the people’s rights are basically the same.

Interestingly, the adoption of cryptocurrencies such as Bitcoin and Ethereum is very high in Nigeria, with over 50% of the population owning crypto. What happened when the government issued a digital currency for the nation? Not much…

Less than 1% of Nigerians supported the local CBDC, even when they were given discounts as an incentive to use the CBDC instead of paper currency or crypto. The ‘carrot’ approach of offering discounts for CBDC use did not work, and the government tried the stick: banks in Nigeria were drained of paper cash to further encourage people to use the cashless CBDC alternative. Riots subsequently broke out in the streets, which is generally not a good look for any government.

We cannot be sure about the success or failure of other CBDC rollouts for the other fifty nations, but we watch with interest to see what happens. It may be that, in countries with less crypto adoption and knowledge than Nigeria, people may be more likely to agree to a CBDC. On the other hand, global CBDC issuance may turn out to be a worldwide fiasco that pushes people further into hoarding paper notes, or seeking a crypto alternative. Stay tuned.

More good news: Bitcoin recognised by Goldman Sachs

In a report this month, Goldman Sachs stated that Bitcoin was the best-performing asset so far in 2023. Of course, the cynics may rush in and claim that it was easy for BTC to bounce up 60-70% after a terrible crash last year, or that crypto is just far too volatile, what with its 80% drops and 1000% gains…

However, the pointy-heads at Goldman Sachs have done the calculations and focused on “risk-adjusted returns”. This is a complex algorithm so feel free to look it up online, but basically, they calculate the performance of an asset and divide it by its volatility. An investment with a return of 10% and volatility of 100 would score lower than an investment that made 5% with a volatility of 20.

As an example, spot gold scored a risk-adjusted 0.8 on the Sharpe Ratio (decent returns, not much volatility) whilst Bitcoin scored 1.9. Yes, Bitcoin’s volatility is far higher than gold, but the overall performance more than makes up for the dips.

For the tech-boffins, here is a link to the full chart and a link to the article.

Recent performance

From cyclical lows to recent highs, Polygon (MATIC) has risen 342% and remains one of our best altcoin buys. We have also seen decent gains in HIVE, Illuvium and Uniswap. Other altcoins are expected to start taking off soon, as historically, the bounce in Bitcoin often takes a few months to reach many of the altcoins. Keep HODLing and tell your friends to get in quick Of course, we cannot guarantee there will be no bumps in the road, but the journey to the next Bitcoin halving in 2024 seems to have started very well indeed.

As at March 31 2023

BOS NAV 67.361842 AU

BOS Price 74.0980262 AU

BOS NAV 46.4796716 US

BOS Price 51.1276387 US

DART NAV 88.5137582 AU

DART Price 97.365134 AU

DART NAV 61.0744932 US

DART Price 67.1819425 US

The Bostoncoin fund is down 60% from April last year, in line with the huge drop in Bitcoin and altcoins after the FTX fiascos of late 2022, but the fund has bounced back up 52% in the three months since 1 January 2023. We are cautiously optimistic about a bumper run for the remainder of 2023.

Bostoncoin three-year growth is a healthy 267% and four-year growth is 228.6%

You may recall that back in the early days of the 2020 pandemic, Bitcoin rose 300% in the three months from Dec 2020 to March 2021, crashed by 50% a few months later in July 2021 and then doubled again to exceed the previous record high by November 2021. In case you had not yet heard, cryptocurrency markets can be very volatile!

Crypto investing is not for the faint of heart, or for those who want to make a quick dollar. We are here because we believe in the technology and the longer-term gains. As they say in the charting world, “if in doubt, zoom on out”. Look for the long-term trends, not just the daily bounces. Despite volatility, incoming regulations and the occasional rogue actors, we still believe that in the next decade, crypto will trend upwards.

See you next month!

JB